The great financial crisis of 2007-2008 made clear the uncertain nature of fair-value valuation of financial instruments, and demonstrated the inadequacy of regulations to mitigate losses which had by then far exceeded equity capital. Uncertainty in this case concerns both model parameters (e.g. choice of volatility curve, discount curve, determination of correlation, etc.) and observed market prices (low liquidity on certain markets, absence of firm prices for certain products).

Fair Value

Fair value is by definition based on the closing price, since it represents the price received for the sale of an asset or the price paid for the transfer of a liability in a normal transaction. At inception, fair value is normally the price agreed at the time of the transaction. Thereafter, it must be based primarily on mark-to-market, and if not, on mark-to-model or mark-to-self, depending on the availability/observability of market data.

Prudent Value

And it was with a view to adopting a more conservative valuation method that in 2013 the EU Council adopted the CRR/CDR IV directive, which introduced the concept of "Prudent Value", which aims to adopt the prudent value to remedy uncertainty in the valuation of instruments at fair value in capital calculations and Basel ratios.

The aim is to obtain a value which, in 90% of plausible scenarios, will enable the position to be unwound. It is this Prudent Value that enables us to obtain the AVA (Additional Value Adjustment) by calculating the difference between the FV and the PV. This gives, for an asset position :

AVA

Consequently, fair value adjustments (FVA) are used in the financial industry to correct the fair value of an asset or liability by taking into account various elements of risk or uncertainty that are not always adequately reflected in market prices. The objective of the CVA is to adjust the accounting valuation of a financial instrument to better reflect its true economic value, taking into account factors such as credit risk, market illiquidity, volatility and other considerations specific to the instrument in question.

There are nine types of AVAs, each taking into account a non-integrated adjustment (when conditions apply) in the FV:

- Market Price Uncertainty(MPU)

- Close-Out-Cost(COC)

- Model Risk(MR)

- Unearned Credit Spread(UCS)

- Investing and Funding Cost(IFC)

- Concentrated Position(CP)

- Future Administrative Costs(FAC)

- Early Termination(ET)

- Operational Risk(OR)

The regulation, which deals with prudent valuation, sets out guidelines for calculating prudent valuation adjustments (PVAs) deducted from CET1 capital in accordance with articles 105 and 34 of the CRR. It specifies that all positions measured at fair value in the banking and trading books are concerned, but offers exclusions for those where a change in fair value has no impact on regulatory capital.

With regard to the calculation of FVAs, the regulation proposes two approaches: a simplified approach for institutions with a portfolio of less than €15 billion, where a single FVA is determined at 0.1% of the absolute aggregate amount of fair value positions, and a principal approach for institutions exceeding this threshold or choosing this method.

Simplified / Standardized approach

Simplified IVA is calculated only once at the level of the institution, and not instrument by instrument or category by category, as in the "core" approach. The calculation method is as follows:

Core approach

It should be noted that there are three different methods for calculating the MVA for each financial instrument, and consequently for each of the categories that will be detailed below:

- The first is based on the generation of different possible scenarios by estimating a series of plausible values for each category of uncertainty, in order to choose the point that we are 90% sure of reaching (Prudent Value).

- The second is when there is a lack of sufficient data to develop a coherent set of values for a given valuation, and establishments adopt an approach drawing on the expertise of qualified individuals. This approach integrates available qualitative and quantitative information with the strategic vision of experts in the field to determine our Prudent Value.

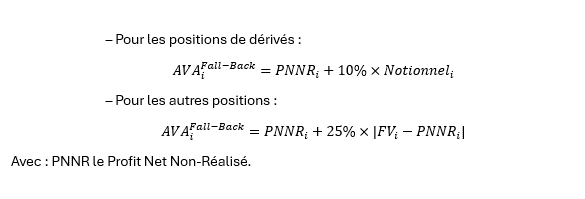

- The third is the "Fall-Back" approach, which will be used as a final solution if we fail to apply the last two methods, and the calculation of the MVA following this approach is carried out as follows:

AVA MPU

This AVA is concerned with the exit price of positions (mark-to-market) and the parameters used in valuation models (mark-to-model). To calculate this type of VAA, we need to generate a series of plausible exit values in order to estimate the PV, which here corresponds to the 90% quantile of these values.

This gives us :

This AVA is zero if, in a liquid two-way market, we are certain of the information available. That is, the information available on the market (transaction prices, firm bids, brokers' consensus and estimates) leaves no significant uncertainty regarding the valuation of the position.

AVA COC

The AVA COC captures the uncertainty (and costs) associated with the impossibility (sometimes) of unwinding a position at the Mid price. In effect, if we are uncertain of being able to close our positions at the market price (Mid), we may incur a margin representing the market illiquidity at the time of closing the position, and consequently incur additional costs charged by our Broker.

To calculate this AVA, we need to construct a series of plausible spreads between Bid and Ask, then estimate the PV of this spread so that we can be 90% sure that this spread will allow us to unwind the position. And in this case :

This AVA is zero if the MPU AVA has been calculated on the basis of exit prices, or if the market is sufficiently liquid for us to be 90% sure of being able to unwind the position at the Mid price.

AVA MR

The MVA in this category takes into account the risk associated with the valuation model that emerges due to the potential existence of various models or calibrations used by market players, as well as the absence of a defined exit price for the specific product being valued.

Wherever possible, institutions calculate the MRVA by simulating a series of plausible values generated from alternative approaches in terms of model and calibration. In this context, institutions determine a point within this series of values where they have a 90% certainty of being able to close their position at this price or at a more advantageous price.

AVA UCS

AVAUCS captures the risk associated with the uncertainty contained in the adjustments made to the valuation of an instrument to reflect counterparty risk (CVA). To ensure accuracy, UCS AVA is subdivided into distinct categories: Market Price Uncertainty (MPU), Closing Cost Uncertainty (COC), and Model Risk (MR). Each subdivision is then allocated to its respective AVA category.

AVA IFC

This particular adjustment is undertaken to take account of uncertainty in the valuation of financing costs used in determining the exit price, in accordance with the applicable accounting framework. Institutions subdivide ICUVA into specific categories such as market price uncertainty (MPU), liquidation cost uncertainty (COC), and model risk (MR). Each of these subdivisions is then reallocated to its respective IVA categories.

AVA CP

This specific type of MVA, called "Individual MVA for concentrated positions", is estimated in three separate steps. First, institutions identify concentrated positions. Then, for each identified position, in the absence of an applicable market price, a prudent exit period is estimated. If this period exceeds ten days, a CVA is calculated, taking into account the volatility of the valuation data, the volatility of the bid-ask spread, and the potential impact of the hypothetical exit strategy on market prices.

AVA FAC

When a total exit of the exposure is envisaged, the institution has the option of assessing a nil AVA relating to future administrative costs. However, if an exposure is unable to demonstrate a nil DALY in accordance with this, institutions calculate the DALY for future administrative expenses (DALY) by taking into account future administrative expenses and hedging costs over the expected life of the exposures involved in the valuation. This estimate is derived using a rate that approximates the risk-free rate.

AVA AND

AVA ET estimates losses relating to non-contractual early termination of customer transactions by taking into account the percentage of such terminations and the resulting losses.

AVA OR

The OR VAA focuses on assessing the risk of potential losses resulting from operational errors in the valuation process. Unlike the other AVAs, it is not calculated at position level, but directly within the operational risk category.

an article written by...

Moataz SABI

Quant Consultant at Quanteam